Unit Three- Financial Choices

5. Lesson Five: Transportation Expenses

- a car depreciates over time and is usually a poor way to make money

- the kind of car insurance you choose will affect the type of coverage you will receive

- your choice of transportation can affect how much money you can save

In the last lesson, you explored the topic of investing your hard earned money. For some of you, saving money for a car is a priority. If it, I want you to think about whether it is better to be buying a new or used vehicle. In this lesson, you will be taking a look at the costs:

|

The Cost of Owning and Operating

a Car

Ownership (fixed) costs:

• Depreciation (based on purchase price)

• Interest on loan (if buying on credit)

• Insurance

• Registration fee, license, taxes, GST

• Service contract (if purchased)

Operating (variable) costs:

• Gasoline

• Oil and other fluids

• Tires

• Maintenance and repairs

• Parking and tolls

• Tickets

Real cost of operating a car

Ownership costs include insurance, finance charges, license, registration,

taxes and depreciation.

Operating costs include gas, oil, tires & maintenance.

Gas just one factor in cost of

owning a car

By Kathleen Pender

Thursday May 29, 2008

The owners of sport utility vehicles and other gas hogs are

feeling particularly squeezed these days. While the cost of filling their tank

is going through the roof, the value of their cars is falling fast. Between March and April of this year, average used-car

prices fell 4.5 percent for large SUVs and 5.6 percent for large pickup trucks,

according to J.D. Power & Associates. They rose 7.3 percent for compact

basic cars such as the Honda Fit, Toyota Yaris or Nissan Versa. A separate study by Kelly Blue Book found that large luxury

cars, such as the Mercedes-Benz S-Class and BMW 7 Series, "are

depreciating even faster than SUVs," says Kelly spokeswoman Robyn Eckard.

She says large luxury cars get the same lousy gas mileage as SUVs - about 12

miles per gallon. But unlike most SUVs, they generally require premium

gasoline. Because depreciation is the biggest cost of owning a car,

people who trade in gas guzzlers for a more fuel-efficient vehicle could wind

up losing more than they save at the pump, according to a new study by Consumer

Reports. This is especially true if they financed the first car and trade it

within three years for a new car. The study highlights the importance of looking at the total

cost of owning a car and not just the soaring price of gasoline. The biggest cost, according to

Consumer Reports, is: depreciation (48 percent),

followed by fuel (21 percent), interest (12 percent), insurance (11 percent),

maintenance and repairs (4 percent), and taxes (4 percent). "The first three years of

owning a vehicle is the most expensive time," says Jeff Bartlett, deputy

automotive editor with ConsumerReports.org. That's because cars depreciate or

lose their value fastest in the first three years and much more slowly in later

years. And if you finance the car, interest will make up a larger percentage of

your monthly payment in the early years and a smaller portion in later years.

Home loans work the same way, although over a much longer period. If you trade in a car before it's

paid off, you might have less "equity" or trade-in value than you

expected. If you swap a 2- or 3-year-old car

for a new car, "you are rushing from the most expensive period of one car

into the most expensive period of the next," Bartlett says. You'll also pay

more taxes, higher licensing fees and, in many cases, more for insurance. Consumer Reports estimated the

total cost of keeping a 3-year-old gas guzzler financed with a five-year loan

for an extra year or two versus trading it in for a new, more fuel-efficient

car. It ran the scenario for a sedan, an SUV and a pickup truck. In all three cases, it was cheaper

overall to hold the guzzler for another year or two. "Even if gas prices

increase to $5 per gallon, our analysis shows trading in after three years

instead of five would still be a hit to your long-term finances," the

report says. Bartlett says it could be

economical to trade in a 3-year-old gas guzzler if you had paid cash for it. If you're buying a car for

environmental reasons, it makes sense to buy the highest-mileage vehicle that

fits your budget and needs. David Jamison of San Francisco

ordered a bright yellow Smart Car - a tiny two-seater made by Mercedes-Benz -

over the Internet about 10 months ago, before even test-driving one. "It's

a visible signal of cutting down gas usage and automobile size," he says.

"We're trying to make a statement but have fun at the same time." But if you're looking for a good

trade-off between fuel economy and overall cost to own, here's what three automotive

experts suggest. -- Jack Nerad, executive market

analyst with Kelly Blue Book, recommends "a high-mileage conventional

vehicle," such as the Honda Civic. Alternatively, "a 2- or

3-year-old Hyundai is a pretty high-quality vehicle, but because it doesn't

have as good resale value, it might be a better deal than a Civic," he

adds. "Taking a contrarian view, if

you need a full-size SUV because you tow a horse trailer or have seven kids,

this might be a great time to buy one. There are a lot of incentives, and you

might find the money you save more than makes up for any fuel cost," Nerad

says. "The best full-size SUVs are

the Chevy Tahoe and GMC Yukon, which have intelligent fuel management systems

that let you operate on four or eight cylinders," depending on need.

"If you look at the number of passengers you can carry, the fuel economy

per person transported is pretty darn good. They only become an issue"

when there's a single occupant. -- Philip Reed, senior consumer

advice editor for Edmunds.com, says gas-electric hybrids get superior gas

mileage but cost more than their non-hybrid counterparts. As gasoline prices rise, the time

it takes to recoup the price premium is shortening for some models, Reed says.

"It's down to 1.6 years for the Toyota Camry hybrid," Reed says. "So much attention is paid to

hybrids that people overlook other ways to get good fuel economy," Reed

adds. "You can get a fairly large family sedan with a four-cylinder

engine, such as the Honda Accord. If you drive it right, you might get 30 miles

per gallon." The newly redesigned Chevy Malibu

"is a very fuel-efficient vehicle, even with six cylinders," he adds. Reed predicts the new Smart Car

"will be a hit initially. It's so cute." It gets good gas mileage and

seats two comfortably. But he says some Americans will dislike the balky,

European-style transmission. -- Bartlett says, "The best

way to improve fuel economy is to buy just the size you need, not a size

bigger." Among hybrids, "the slam dunk

now is the Toyota Prius." Among regular sedans, the Nissan

Altima with a 2.5-liter, four-cylinder engine is "a fantastic option. It's

a top-rated car by Consumer Reports and also has among the highest fuel economy

in its class. It's really entertaining to drive." For large families, he recommends

minivans, such as the Honda Odyssey or Toyota Sienna, over SUVs. Both get about

19 miles per gallon. "One interesting alternative

that deserves attention is the Mazda 5. It's a cross between a station wagon

and a minivan," he says. It seats six in three rows and in Consumer

Reports tests got about 23 miles per gallon.Add up the costs

Recommendations

WHAT ARE YOU WAITING FOR?

According to news reports, large numbers of twenty- and thirty—year-olds are migrating back to their parents’ houses where they get a free roof over their heads and free use of the TVs, VCRs, gym equipment, and so forth. This trend is supposed to indicate that America has produced a new generation of freeloaders, who lack the gumption to go out into the world and make it on their own. There’s a good side to this that we haven’t heard much about, except in a recent headline in The Wall Street Journal: “Generation X Starts Saving for Retirement.”

The gist of the story is that the freeloading twenty-something’s who belong to

the so-called lost generation, or Generation X, have been quietly stashing away

their loot. Apparently, there are more savers in this group than among their

parents, the baby boomers who prefer buying things now to saving money for

later. The Xers have realized that they can’t count on social security to bail

them out. They’ve watched their parents struggle to pay off credit-card debts,

and they want to avoid repeating this mistake. They seek financial

independence, and they’re working toward it while they’re still at home, with

their parents picking up the tab.

This is a very positive development, and we can only hope that more teenagers will follow in the footsteps of the twenty-something’s and not fall into the familiar trap of buying an expensive car. Many kids can’t wait to do this. As soon as they land that first steady job, they become slaves to the car payments.

It’s cool to drive around in a flashy new Camaro instead of a used Ford Escort,

but that kind of cool is very costly in the long run. What’s the price of cool?

Consider the following two cases:

Joe and Sally

Joe gets a job as a clerk at Wal-Mart. He’s living at home and saving every

last dollar so he can make the $2,000 down payment on a $20,000 Camaro with the

racing scoop on the hood. He takes out a car loan for the remaining $18,000.

His parents have to sign for the loan, but Joe is making the payments. It’s a

five-year loan at 11.67 percent interest, so he sends $400 to the finance

company every month. He cringes the first time he seals the envelope, kissing $400

goodbye, but he forgets all about that when he’s driving around in the Camaro

and his friends are telling him what a cool car it is.

A few months later, there are scratches on the door and stains on the carpet

and nobody is oohing and aahing when the Camaro pulls into the parking lot.

It’s just another car by now, but Joe is stuck with the payments. To be able to

afford the car and a date to ride in the car he works an extra night shift,

which means he’s too busy to get many dates.

At the end of five years, he’s sick of the Camaro, which lost its cool a long

time ago. He’s finally paid off the car loan, which cost him an extra $6,000 in

interest charges, so between the loan and the original purchase price, Joe has

invested $26,000 in this car, not including taxes and fees, insurance premiums,

gas, oil, and maintenance.

At this point, the Camaro has dents and stains and the engine sounds a bit

rough. If he sold the thing he could get maybe $5,000 for it. So what he’s got

to show for his $26,000 investment is a $5,000 car that he doesn’t even like

anymore.

Sally also lives at home and works the Wal-Mart checkout line a few feet away

from Joe, but she didn’t buy a cool car. She took the $2,000 she’d saved up and

bought a used Ford Escort. Since Sally paid cash, she didn’t have car payments.

So instead of sending $400 a month to the finance company, she invested $400 a month in a

mutual fund for stocks.

Five years later, when Joe was mailing out his last car payment, the value of

Sally’s mutual fund had doubled. Between the doubling of the fund itself and

the steady stream of $400 contributions to the fund, Sally has an asset of

nearly $30,000. She also has the Escort, which gets her back and forth OK, and

she never worries about the dents and stains because she never thought of her

car as an investment. It’s only transportation.

Automobile insurance policies are basically similar in nature and the companies that issue them are strictly controlled by government regulations. It is always a good idea to read the policy carefully clause by clause, to make sure you fully understand all of the conditions of the agreement before you sign it.

• The second section covers accident benefits to drivers’ passengers. Often,

where both parties to an accident are insured, the insurance companies will

agree not to take court action to establish responsibility. This “no-fault”

plan saves the insurance company administrative costs and court time.

• The third section gives protection to the owner against possible damage to

the vehicle. Next to your home, your automobile may be the most expensive

property you own. You stand to lose a great deal if your vehicle is damaged in

an accident or through fire, theft, acts of malice, accidental windshield

breakage, etc.

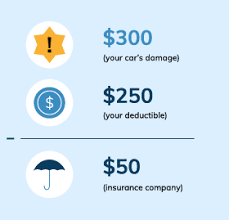

Deductible clause

You probably heard of $100-deductible or $250-deductible insurance. Insurance

premiums would be much higher if the insurance companies were to pay for every

scratch or dent that occurred. To lower costs, most policies include a

“deductible clause”. This clause means that if the vehicle were damaged, the

first $10 or $250 of the repair costs will be borne by the insured and the

balance will be paid by the insurance company.

Automobile insurance rates

Insurance rates vary according to five factors.

Your locale. Rates in each province differ and they even vary from city to city

within the provinces. Usually, they are higher in areas where traffic is heavy

and lower in rural areas where traffic is light. In regions roads are hazardous

in winter, rates can be higher than where roads are dry.

Your classification. There are three classifications.

• The car is owned and driven by an adult over the age of 25;

• The principal driver of the car is over 25, but it is also driven by a young

adult under 25;

• The principal operator is under 25.

A male driver who is under 25 belongs to the driver category with the worst

accident record. Premiums are highest in this category. When he gets older and

establishes a record of driving without accidents, or without major traffic

violations, his premiums will be substantially reduced. Some insurance

companies give a discount if a new driver has completed an approved driver-

training course.

The use to which the car is put. There are three classifications.

• The car is used for business only.

• The car is used to drive to and from work.

• The car is used for pleasure only.

*Premiums are lower to mainly for pleasure rather than for business. The number

of kilometers driven is another factor taken into consideration.

Your driving record. A person who has a bad accident record or has been of

major traffic violations will have to pay more than the regular premium rate.

The make and age of the car. When a policy holder automobile is totally damaged

in an accident, the amount paid by the insurance company will depend on the

value of the car at the time of the loss. The car value depends on such things

as make, model, age and condition.

Uninsured motorist coverage

All provinces have passed legislation setting up “unsatisfied judgment funds”

to provide at least a minimum payment of damages in automobile accident claims

where the person responsible for the accident carries no insurance. The fund

sometimes allows for the payment of damages for injuries in hit and-run

accidents.

If an uninsured motorist is at fault in an accident and the victim receives

payment from the unsatisfied judgment fund, the motorist generally will be

called upon to reimburse the fund for the amount paid. Failure to repay the

fund may result in suspension of the driver’s license.

**Many Insurance companies are now adding an additional clause to motor vehicle

coverage called Uninsured Motorist Coverage

Exploring Transportation Alternatives

North Americans have a continuing love affair with the automobile. The great distances between centres of population, the personal convenience of coming and going as one pleases, and the relatively inexpensive nature of owning and operating a car contributed to this affair.

In recent years, the cost of fuel

has increased

dramatically. Concern over environmental pollution

by engine exhaust is also mounting. In response to

government pressure and the demand of customers, the automotive industry has made changes in the size. efficiency. and safety standards of cars produced in North America.

The cost of new cars has risen

dramatically in recent years. The cost of servicing, repairing, and insuring

them has

increased as well. At some point one questions the trouble and expense of owning and operating a car. People are seeking alternatives.

It makes sense for young people, in particular, to examine alternatives to owning a car. Borrowing money to buy a car is expensive. Also, insurance rates for young people are higher than for any other age category. You can expect to pay from $1200 to $4,500 or more per year for insurance. The average annual cost of owning a car according to the

Canadian Automotive Association is $10560 if driven 24,000 km annually. These costs are outlined in their pamphlet, 2004 Driving Costs.

*Canadian Automotive Association figures are based

on the cost of operating a midsized North American car in Alberta. The figures do not reflect the higher costs of

insurance that a person under 25 would

have to pay.

Get all the information on the current costs before you make your decision.

Let's take a look at some other ways of spending

these transportation dollars.

Public Transportation

In cities, transit passes are available for $83/month

which is $8230/year. Still less expensive than owning a car and parking it. If

your work and home connect well with bus routes and scheduling, consider this

good alternative. You have no parking costs or tickets, no gas, oil or

servicing, and no tension from the traffic jams. You can read the papers, daydream, and enjoy yourself.

Bicycle

A bike can be purchased for $300 to $500. It is an

adventurous way of travelling in spring, summer and

fall. Nothing is more fun in traffic jam than a 10 speed bike!

Taxis

The bus or rapid transit system is not always

convenient. Shopping for groceries and going out in

the evening require more convenient forms of

transportation. Taxis are one option. Even allowing

$25 per week for taxis, the yearly total is $1300 less

than the cost of insurance for most young

people.

Holidays

Do you like to ski or snowboard? Jasper for the weekend from Calgary by bus at $194.50 plus tax, return is an interesting possibility. Perhaps you prefer Banff at $51.20 plus tax, return.

Let's say you take three trips by bus to Jasper and

two to Banff. The total cost is less than $750.

Longer Holidays

What about a long weekend in Las Vegas? Three days and four nights including air transportation, transfer between airport and hotel and accommodation comes to about $860 including tax.

In recent years, the cost of fuel has increased

dramatically. Concern over environmental pollution

by engine exhaust is also mounting. In response to

government pressure and the demand of customers, the automotive industry has made changes in the size. efficiency. and safety standards of cars produced in North America.

increased as well. At some point one questions the trouble and expense of owning and operating a car. People are seeking alternatives.

Canadian Automotive Association is $10560 if driven 24,000 km annually. These costs are outlined in their pamphlet, 2004 Driving Costs.

on the cost of operating a midsized North American car in Alberta. The figures do not reflect the higher costs of insurance that a person under 25 would

have to pay.

these transportation dollars.

Bicycle

A bike can be purchased for $300 to $500. It is an

adventurous way of travelling in spring, summer and

fall. Nothing is more fun in traffic jam than a 10 speed bike!

Taxis

The bus or rapid transit system is not always

convenient. Shopping for groceries and going out in

the evening require more convenient forms of

transportation. Taxis are one option. Even allowing

$25 per week for taxis, the yearly total is $1300 less

than the cost of insurance for most young

people.

Holidays

Do you like to ski or snowboard? Jasper for the weekend from Calgary by bus at $194.50 plus tax, return is an interesting possibility. Perhaps you prefer Banff at $51.20 plus tax, return.

two to Banff. The total cost is less than $750.

What about a long weekend in Las Vegas? Three days and four nights including air transportation, transfer between airport and hotel and accommodation comes to about $860 including tax.

Vacation

A good time to holiday in the

tropics is in the summer. Airfares and accommodation costs are low. Summer in Hawaii including seven days on Oahu and six days on Maui, with airfare and hotel accommodation, comes to about $3,000 if you can find a friend to travel with you.

Or take an offseason charter to Europe for $1000

airfare. The cost goes up in the summer months and

during Christmas holidays.

With the cost of bus passes,

taxis, a bike, five trips

to the mountains, a long weekend in Las Vegas and

a holiday to Hawaii or Europe, you will still spend

less on transportation than it costs to own and

operate an average car in Canada for one year.

Consider the alternatives to owning and operating a

private car.

puff and a lemon, you'd better stay away from the

used car market. These terms are used by salesmen to describe a delicious car in excellent shape or one that will sour on you. It takes more than luck to buy a cream puff. The following pointers will help you!

Will the money be well spent with your car giving

hours of enjoyment and pleasure? Or will you be

short of money for other things? Think of food,

clothing, shelter, dates, travel, and holidays. If your

car is going to be your main hobby and interest, you

may want a more powerful, expensive car. But know

what you are getting into. If you choose a sports

car, be prepared to spend a lot of money on purchase, interest, insurance, and repairs.

Before you start looking for a car decide how much

money you can afford to spend. Be sure that the

money would not be better spent attaining a more

important goal.

DO YOU REALLY NEED A NEW CAR?

According to Runzheimer, the average new compact cost about $7500 to run

last year. For a minivan, the price rises to around $ 8,400. The major expense

items are depreciation, gas and interest paid on financing. What the numbers

tell you is that the best way to save is not to buy a car! That is, the best

way to reduce depreciation and financing is to keep your old car longer or buy

a used vehicle. A two- or three-year-old car will have depreciated

considerably- by as much as 50% for some models, and financing and insurance

will be lower. When it comes to reducing fuel costs, the largest actor is how

much driving you do, followed by the vehicle’s fuel consumption.

The older used car will need more maintenance and repairs, and it may he in the shop more often. But the sayings easily outweigh the extra expense, and you should come out ahead at least $2,000 per year- more if it’s a second car you don’t plan to drive as often.

-You’re buying a new car: Obviously... but not necessarily! You might be

signing a lease, in which case ownership does not change hands. In today’s

depressed market, dealers make less on new cars than you think. Alter

negotiation, mark-ups range from zero to about 10%- figure about $500 to $

1,200 depending on the price of’ the car and your negotiating ability.

-Options: Almost no one buys just the basic model. Options can be bought

individually or as part of option packages. Factory options are marked up in

the 15% range. Dealer-installed options, like deluxe floor mats, racks and

radios, are marked up 30-50%. Add $100 or more profit, depending on the options

and the deal.

-You’re selling an old car: Your trade-in provides additional revenue for the

used car department. Depending on the pricing strategy, your trade will add

zero to $2,000 or more profit to the deal.

-Financing: A service you’ll probably be “purchasing”, either I win the dealer,

manufacturer, or a leading institution. Most people don’t look at financing as

a profit-maker for the dealer, or they think that financing is a generic item

with a generic price, but that’s not the case. The dealer passes on your

financing contract to the lowest bidder, usually a bank, and pockets the extra

interest you were charged, called the ‘‘spread” in industry jargon. I. easing

is an alternative wav of financing that is more profitable. Profit ranges front

about $150 to several hundred dollars, depending on the amount financed, the

duration of the loan and how well you shop.

-Loan insurance: Pays off your remaining payments in case of death or long—term

disability. It’s usually tacked on to your loan. Price varies greatly depending

on buyer smarts and seller integrity. It can add anywhere trout $50 to many

hundred dollars profit to the deal.

-Rustproofing: A dealer supplied service with a mark-up of 100% or more, for a

profit of $150 to $200. According to a recent CAA study, over 80% of dealer

rust-proofing is poorly applied. (In Ontario and Quebec, contact the APA for a

recommended aftermarket rust-proofer.)

-Paint sealer, upholstery protector, tire sealant: Other dealer supplied

services which usually have mark-ups in the 200-400% range. Add $200-$300

profit for the paint sealer, and $50-$75 each for the tire sealer and

upholstery spray. These services are usually available for much less at an auto

detailing shop. The APA does not recommend tire sealer and a can of Scotch

guard will protect fabrics as well as the cheaper generic product the dealer

uses.

-Extended warranty: Extra-cost coverage for mechanical failures. Dealer

commission for selling is usually 25-35%. It’s not necessary for most cars in

the APA’s recommended category.

-Liability and collision insurance: Relatively new arrivals to Canadian

dealerships. Commission varies, and it is often quite small. But dealership

collision insurance is often built into your finance payments, so interest

profit is possible.

-Extras: Auto club membership, plane tickets to a far-away destination, “free’’

first month’s payment, “free’’ bicycles, “free’’ automatic transmission or air

conditioning. In most cases, you’re paying for all or part of the cost of these

items.

Here’s a look at some of the strategies you can use to improve the odds of

driving a good bargain.

Nowadays the best of the compact cars should fill just about everyone’s needs. They’re comfortable for four or five people, handle well, are relatively fuel efficient and quiet. If safety comes first and you budget permits, it still pays to go for one of the big bomber with a good safety record made by Mercedes Benz, Volvo or Ford. If a low purchase price and economy of operation are paramount, look at the small cars section. This process may seem obvious, but be aware that people who don’t do it are easy to diver in the showroom. If you buy the sharp looking two-door that incidentally paid the salesperson a higher bonus instead of the four-door you really needed, you’ll be reminded of it every time you let someone into the back seat.

Car buff magazines are mainly for car buffs. They provide a fairly complete

description of the car’s technical features and road test data oriented toward

performance. But forget about reliability or resale. The car buff magazines get

their cars free from the auto makers- usually very well equipped models with

low mileage. Cars are kept for a couple of weeks and then returned. Gas and

speeding tickets are usually the only things paid for by the magazine.

Occasionally a car is kept for a “long-term evaluation”, say six months. But that’s

still nowhere near as long as a consumer owns a car, and most repairs are

covered by the warranty. To really get the handle on reliability, service and

retail, you have to listen to car owners.

The best road tests to look for are comparison tests which match cars in the

same class and price range against one another. Without that comparison, a test

has no context. For example, what good is it to know that the Ford Mustang has

a cramped back seat, if you don’t know that competing sporty cars are even worse.

Among the American buff magazines you’ll find on the newsstand, Automotive and

Car and Driver have the best customer information. Popular Mechanics and

Popular Science are also worth looking at. Although not exclusively devoted to

cars, these magazines regularly perform comparison tests.

Try to estimate how much you can comfortably pay each month. Many consumers

only look at monthly payments and that’s how they wind up paying far too much.

Monthly payments can be reduced so many ways, that payments alone are not

reliable indicators of whether you’re getting a good deal. A salesperson can

sell you a cheaper car or reduce the interest rate to bring down the monthly

payment. But it’s just as easy to increase the length of the loan or the amount

of down payment. In these cases, lowering the monthly payment actually

increases the cost of financing.

The cheapest solution is to pay from savings. Here’s why: at present, interest rates on bonds and term deposits are around 6%. The interest income is taxable, so you’ll likely only keep about 4%. So, if you pay from savings, you’ll lose about 4% in interest income. That’s much cheaper than the 9-10% you’ll pay on a well — negotiated loan. Even if your investments pay a better rate of return than bonds, you’d have to be earning at least 15% a year (reduced to about 10% after taxes) to come out ahead by taking out a loan. If you don’t have enough money to pay cash, set aside the largest down payment you can reasonably afford. And to lower the cost of borrowing, try to pay back the loan in the shortest time possible. That way more dollars go to reducing the loan principal and fewer to interest.

What about below-market interest discounts from the automakers, say 2.9% or

even 0%? The automaker or dealer has to make up the difference between the

reduced rate and prevailing market cost of borrowing money. The cost may be

passed on to you in the form of a higher mark-up on the car. The best strategy

is to find out how much of a cash rebate you can obtain instead of the interest

subsidy and then compare the total cost of borrowing for the two plans.

Shop for your loan at a bank or credit union. Most people live in fear of

applying for credit. and dealerships know and exploit that fear. In fact the

worst risks are usually the easiest marks, because they d pay just about any

rate to avoid asking for a loan from their banks. Tell the lending officer that

you’re shopping for a loan. You don’t actually want to borrow the money right

away, but would like the loan approval ready for the day you ink the deal for

the car. You’ll be provided an interest rate and monthly payment schedule.

These are helpful, but they don’t tell the whole story. Find out the total cost

of the loan including interest charges and credit insurance.

What you want is the total cost of the loan. If you have securities or bonds,

ask if you can pledge them to lower your interest rate a bit. Generally,

choosing a variable

interest rate loan is a bit cheaper than a fixed rate, but your interest

payments will follow the market.

Monthly payments are somewhat lower with a lease because you’re not paying off

the whole value of the car if you choose to purchase it there’s always that

buy—back to pay at the end. With a traditional loan, you own the car outright

when the last payment is made. When you add up the cost of the monthly payments

and the buy—back, leasing is nearly always much more expensive than financing.

It. this were the only pitfall, leasing wouldn’t be that risky — just an

expensive way to use a car. But it doesn’t end there. Leasing cars to consumers

is fairly recent, so it has escaped lending legislation designed to protect

borrowers.

Here are some

of the dangers:

- Most leases do not tell you the true annualized

percentage rate. The lessor has to borrow the money to it finance your car, but

many dealers jack up the rate. When the APA analyzed leasing contracts for

Consumer and Corporate Affairs some years ago, the interest rate on leases was

frequently in the 15%—23%range. But buyers hadn’t asked (or that information

and the law doesn’t say the dealer has to tell them.

- A loan can he paid off without penalty if your car is

stolen or written off alter an accident. Prepayment with no penalty or a small

charge is guaranteed under federal and provincial law. Not so with leasing — if

your car is destroyed many leases hit you with the same clauses used against

so—called “deadbeats’’ (in industry parlance, customers who are unable to make

payments). You’ll pay penalties of several hundred dollars for “unearned

profit” or “unearned payments” to break the lease, even if the car doesn’t

exist any more through no fault of your own.

The Province of Québec has introduced tighter controls on leasing practices,

hut it’s too early to say if they’ll have the desired effect. Until the other

provinces do the same, or the industry introduces consumer-friendly contracts,

leasing is probably best left to the professionals. If you own a business, your balance sheet may

look better if you lease the car instead of financing it — hut that’s a

decision for your financial advisor or accountant, not the dealer. The old

argument about getting better tax deductions when you lease is a red herring,

since changes in the law have put buying a car on the same footing

1. How much can you put down? This is important because most lending institutions will only finance a certain percent age of the vehicle’s value.

2. How much can you afford to pay on a monthly basis? A comfortable monthly car

payment will ensure you peace of mind.

3. What are your other costs of car ownership? Besides your monthly payment

there are other factors to include in your budget:

• insurance

• Maintenance (oil changes, tune-ups, etc.)

• license plates and registration

• repairs

• gasoline and oil

* The dealership salespeople are an excellent source of information and can

provide you with brochures on your favourite model to take home and study.

* Consulting the newspaper and magazine ads is a useful tool to determine which

vehicles fall within your price range. Be sure to consider options, rebates,

financing offers, etc., in order to perform true comparisons.

* The public libraries and book stores carry several resources on this subject.

Choosing your Sales Representative is also equally important. You deserve someone fair, honest and knowledgeable. A tip that some people use is to look in the newspaper ads for the dealer’s Top Salesperson Award winners. This person is probably so successful because he or she has a lot of satisfied customers. You have already determined your needs and budget. Share this information with your salesperson; it will save both of you a lot of time.

The sales person’s job is to work with you, the customer and the dealership, to

give you the best value possible. But, it is the sales manager who makes the

final decisions on price.

North American statistics indicate that the gross profit on cars over the last

few years is in the range of 6 - 8 per cent. Expenses such as overhead,

advertising, salaries, and commissions are all drawn form this amount. This

does not give dealers or their sales managers a great deal of elbow room.

Make Sure There’s No Surprises!

The old saying, “Ignorance is bliss” does not hold true for vehicle purchases.

Many anxious moments, misunderstandings and disputes can be prevented if you

follow the golden rule: Ask Questions!

For example:

Warranty:

• What does and doesn’t it cover?

• What is the deductible?

• What is the term in months and kilometers?

• What are your maintenance requirements in order for your warranty to be

applicable?

Leases:

What will be the residual value at the end of your lease term?

Are you obligated to purchase the vehicle at the end of your lease?

Are you allowed to sub-lease the vehicle?

What are the terms and conditions of the lease agreement i.e. time frame,

mileage restrictions, and deposit, insurance and maintenance requirements?

What are the dealership’s criteria for assessing the vehicles condition upon

its return?

What happens if you miss a payment?

Payment:

Does your monthly payment include:

• Life & disability insurance?

• Fabric guarding?

• Extended warranties?

• Undercoating?

• Rustproofing?

You will be asked to complete an Offer to Purchase and in most cases to pay a

deposit. A deposit is essentially a promise to pay for the product described on

your agreement. If you have any conditions under which you will not purchase

the vehicle and would require the return of your deposit, clearly state the

conditions on the written contract.

Guaranteed freedom from liens and encumbrances. As a result of this guarantee,

the dealer is responsible for all previous claims against the vehicle; unlike a

private sale where you assume 100% of the risk.

Last year there were 8301 vehicles reported stolen in the City of Edmonton alone.

Many of these vehicles are resold to unsuspecting buyers. EMDA members have

demonstrated full protection to any customer who inadvertently acquires a

stolen vehicle from any member dealer.

Security of dealing with an established business. Should a problem arise, you

have the opportunity to work it out with a legitimate business committed to

customer service. The dealer has a vested interest in your satisfaction, the

private individual does not.

Convenience. The dealership essentially offers “one-stop shop ping”. You can

compare several different vehicles at one location and in most cases the dealer

can arrange financing. Your valuable time is saved and frustration is avoided.

Full disclosure. When purchasing a vehicle from a dealer, the vehicle’s known condition

is included in the agreement.

Extended Warranties. Unlike private individuals, licensed dealers can offer

extended warranty packages designed to be a safe guard against major costly

repairs.

Reconditioning. After purchasing a vehicle privately, you could be faced with

added costs such as cleaning, tune-ups, new tires, etc. Most vehicles purchased

from dealers have already been through a reconditioning process. Ask your

salesperson about which repairs have been preformed and ask to see copies of the

work orders.

Some of the advantages to purchasing your used vehicle from a dealership are:

No matter where and from whom you decide to purchase your used vehicle, you

should carefully inspect the vehicle before you buy it. Remember, you are not

buying a new vehicle so expect some problem areas. When you go shopping, take

this checklist with you. It will help you make an informed decision.

Check the vehicle’s exterior

• New paint on a late model

• Ripples in the body

• Misaligned wheels and car body

• Misaligned doors, hood, or trunk lid

• Black smudges or gummy material inside the tailpipe

• Worn shock absorbers

• Unevenly worn tires

• Premature rust

• Drips under the car

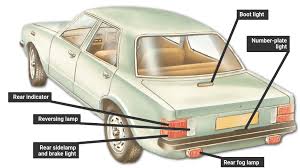

Check the vehicle’s lights

• Interior and dashboard lights

• Headlights including dimmer switch

• Brake lights

• Turn signals

• Emergency flashers

• Parking lights

• Back-up lights

• Rear license plate light

Check the vehicle’s interior

• Over 5 to 7 cm of slack in the steering wheel

• Gas pedal sticking

• Brake pedal with little resistance

• Parking brake not working

• Door locks not working

• Windshield wipers & washer not working

• Seat belts worn or loose

• Worn upholstery or sagging seats

• Seats that won’t adjust

• Damaged windows or winding mechanism not working

• Heater/defroster not working

• No spare tire or tools

• Options not working, e.g. radio, tape player, air conditioning.

Check how the vehicle idles

These points could spell trouble

• Sluggish starting

• Rapid, noisy idle that may hide other noises

• Slow engine response to pressure on gas pedal

• Unusual engine noises, e.g. chatter, knocks, pings

Take a test drive

• Always test drive a vehicle prior to purchasing. If possible drive it in the

city and on the highway, and take a friend along to help.

• How to choose the right car for your needs

• How to protect yourself from buying a lemon

• How to make an offer and complete the sale

• About insurance requirements

Before you buy

Think about why you want a ca Will you use it for city driving only? Or for

long trips as well? How many passengers will you have? Will you need to pull a

trailer or a boat?

These questions will help you to decide on the size and model that will best

meet your needs, and what options are important to you.

Stay within your budget

How much can you afford to pay for a used car? Do you have enough money to

cover yearly costs? These expenses include:

• Registration and license plates

• Insurance

• Gasoline and oil

• Maintenance and repairs

• Parking

• Interest if you buy on credit

Shop around

When you buy a used car, you’ll be faced with a choice of hundreds of makes and

models. Get as much information as you can about the reputation and repair

records of different cars. This information is available in most public

libraries and book stores. Some guides to look for are Lemon-Aid Used Car Guide

and Consumer Reports Guide to Used Cars. Useful magazines include Canadian

Consumer; Protect Yourself, and Consumer Reports.

Research car prices by studying classified ads in newspapers and specialty

publications that sell used goods. Some titles to look for are Auto Trader and

Bargain Finder. Also check the public library for the Gold Book of Used Car

Prices and the Canadian Red Book.

If you don’t know much about cars, it’s a good idea to shop with someone who does. Try to visit several dealers. Also look for private sales in classified ads in newspapers and the publications listed here.

When you find a car you like

When you find a car you like, inspect it carefully inside and out:

• Look for signs of an accident. Does the hood close properly? Are paint and

chrome new? Any dents?

• Check parts and accessories, such as lights, horn, seatbelts, radio, heater,

and windows. Do they work?

• Look for rust damage.

• Does the car need new tires? Is there a spare?

Remember that most used cars are sold “as is.” That means the seller will not

fix any flaws or damage.

Take a test drive

When you turn on the engine, does it start right away? Are there any unusual

noises or vibrations?

Always test drive a car before you buy it. If possible, drive it in the city

and on the highway, and take a friend along to help. Here are some things to

look for:

• Are the gas and brake pedals firm? When you take your foot off, do the pedals

spring back?

• Do the brakes work well?

• Does the tailpipe produce heavy smoke?

• Does the car steer straight? Is it comfortable to drive?

See a mechanic

Before you decide to buy a car, take it to a mechanic or car clinic for an inspection. One or two hours of a mechanic’s time cost about $50 to $100. This will be money well spent, especially if you discover the car needs costly major repairs (See Make an Offer).

Watch out for curbers

Watch out for curbers. Curbers sell cars from their homes, often leading you to

believe that they are selling their own family vehicle. What they are really

doing is buying used cars for low prices and selling them right away for a

quick profit. A curber is running a used car business without a license. This

is illegal.

If you deal with a curber, you may pay too much. Or you may not be told the truth about the car. For example, a curber may tell you a car has been in his family for years, and was used only on weekends. In reality, it may have been a taxi.

Although it can be difficult to find out if you are dealing with a curber,

these steps can help:

• Check the name of the registered owner on the car’s registration. If it is

not the same as the seller’s, be careful. The seller could be a curber.

• Also check the issue date of the registration card. It will tell you how long

the seller has been the registered owner of the car.

You can also check at a Motor Vehicles Office to find out if the seller is the

registered owner. Write or go in person. You will need the name of the private

seller and the make, year, and serial number of the car. You will have to pay a

small fee.

Check for liens

As a last step before you buy a used car, check for liens. A lien usually means

that a previous owner still owes money on the car. If you buy a car with a

lien, you might

have to pay the amount that is owing, or the car could be legally seized by the

Sheriff.

You can check for liens registered in Alberta by having a search done at the

Personal Property Registry. You will need the car’s year, make, and serial

number. You’ll have to pay a small fee.

Personal Property Registry 5th Floor, I.E. Brownlee Building 10365—97 Street

Edmonton, Alberta T5J 3W7 427-5104

Personal Property Registry 3rd Floor, JJ. Bowlen Building 620—7 Avenue SW

Calgary, Alberta T2P 0Y8 297-6230

If you decide to buy

Satisfied that you’ve found a good used car? Then it’s time to make an offer.

Most dealers, and some private sellers, will ask for offers in writing. The

seller may provide a form, called a Bill of Sale or Offer to Purchase. These

forms are also available from your nearest Motor Vehicles Office.

Make an offer

Be sure you really want the car. If the seller accepts your offer, the car is

yours. Both you and the seller should sign the offer.

You may want to add conditions to your offer. For example, you may state that

your mechanic must inspect and approve the car before the sale is final. If you

need to borrow money to buy the car, you may want to make the offer subject to

getting credit at a reasonable rate.

In these cases, the seller may ask you for a deposit. Write into the offer that

your deposit will be refunded if the mechanic does not give his approval, or if

you don’t receive credit.

Shop for credit

If you’re borrowing money to buy a car, shop around for the lowest interest

rate. Then make the biggest monthly payments you can afford. This will reduce

ihe total amount you pay for the car in the long run.

A credit contract should include:

• A description of the car

• The amount of any trade-in

• Complete financial information, including the total amount owing, the down

payment, the total interest charge, the amount of each payment, the number of

payments, and when each payment is due.

Get a bill of sale

Be sure to get a bill of sale. It should contain this information:

Date of the sale

• Your name and address

• The seller’s name and address

• The car’s year, make, model and serial number

• The number of kilometers on the car

• The price and how you are paying

Ask the seller to write down any important promises or statements about the car. For example, write down any promise about a warranty. If the seller says the car has a new engine, ask him to write that information on the bill of sale.

Get insurance and plates

In Alberta, car owners must have motor vehicle liability insurance of at least

$200,000. If you hurt someone or damage property in a car accident, this

insurance will pay for the costs. If you drive without this type of insurance,

you are breaking the law and could be fined up to $2,500.

When you buy insurance, the agent will give you a pink liability insurance

card. Take your bill of sale and the pink insurance card to a Motor Vehicles

Office to register your car and get license plates. You will pay about $80 for

basic license plates and registration.

Liability (40—50% of premium)

• Bodily-injury coverage

• Property-damage coverage (i.e., to another person’s car)

Collision (up to 30% of premium)

• Pays for the physical damage to your car as a result of an accident

• Limited by deductible

Comprehensive (about 12% of premium)

• Pays for damage caused by vandalism, hailstorms, floods, theft, etc.

Medical

• Covers medical payments for driver and passengers injured in accident

Rental reimbursement

• Pays a specific amount per day to rent a car while yours is being fixed

Towing and labor

• Age

• Gender

• Marital status

• Personal habits (i.e., smoking)

• Type and frequency of vehicle use (i.e., commuting)

Geographic location [classified by postal code)

• “Rural” usually lowers rates, “urban” usually raises rates

Driving record

• Accident with death, bodily injury, or property damage may trigger a

surcharge on premium for 3 years

• Number and kind of moving violations (and total of associated points)

• Number of years insured with the company

Vehicle characteristics

• Damage, repair, and theft record of type and model of car

• Age of car